Embarking on the journey of understanding How Do Title Loans Work In Mississippi? can be a maze of regulations and financial considerations. This article aims to unravel the complexities, offering you a clear guide on what to expect. Let’s delve into the nuances of these loans, starting with the crucial aspect of responsible borrowing strategies.

Key Takeaways

- Title loans in Mississippi offer quick cash using a vehicle as collateral.

- Interest rates can be high, making it a risky option.

- The loan amount depends on the car’s value.

- Repayment terms vary and may lead to repossession if not met.

- It’s essential to understand the state’s regulations governing these loans.

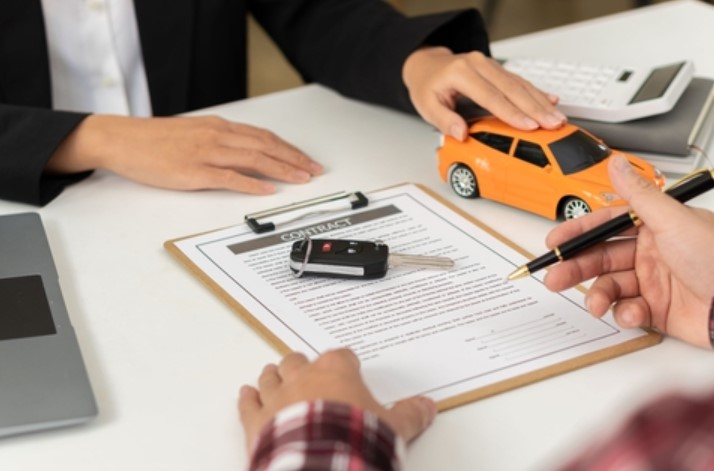

How Do Title Loans Work In Mississippi?

Title loans in Mississippi are a type of loan where borrowers use their vehicle as collateral. It’s a simple process:

- Bring your car and its title to a lender.

- The lender assesses your car’s value and offers a loan based on this value.

- If you accept, you hand over the car’s title and get the loan amount.

The reason title loans are popular is their speed and accessibility; they often don’t require a credit check, and you can get the money quickly, sometimes on the same day. However, they come with high-interest rates, and if you can’t repay, you risk losing your car. This type of loan is governed by the Mississippi Title Pledge Act, which sets out specific regulations and borrower protections.

Understanding Title Loans in Mississippi

Title loans in Mississippi are short-term loans where a borrower’s vehicle title is used as collateral. These loans are a quick way to get cash, but they come with high interest rates and risks. The amount you can borrow generally depends on the value of your vehicle. It’s essential to understand the terms and conditions, as failure to repay the loan can result in losing your vehicle.

How the Process Works?

The process begins with the borrower presenting their vehicle and its clear title to the lender. The lender assesses the vehicle’s value and offers a loan amount based on a percentage of this value. Once the borrower agrees, they must hand over the vehicle title, sign a contract, and receive the loan amount.

Interest Rates and Fees

Interest rates for title loans in Mississippi can be steep. It’s not uncommon to see annual percentage rates (APRs) exceeding 300%. Besides interest, there may be additional fees, including processing or documentation fees.

Legal Aspects of Title Loans in Mississippi

Mississippi has specific laws regulating title loans. These laws dictate interest rates, loan terms, and borrower protections. Understanding these regulations is vital to ensure you’re not exploited.

State Regulations

Mississippi’s Title Pledge Act governs title loans. It caps loan amounts and interest rates and defines the maximum loan term. Lenders must be licensed and comply with these regulations.

Borrower Protections

The state law provides protections for borrowers, like limitations on the repossession process. If a borrower defaults, the lender must follow a legal process before repossessing and selling the vehicle.

Risks and Considerations

Title loans in Mississippi are risky due to high-interest rates and the potential loss of your vehicle. It’s essential to consider these risks and explore alternatives before opting for a title loan.

High Risk of Losing Your Vehicle

If you cannot repay the loan, the lender has the right to repossess your vehicle. This risk makes it crucial to have a solid repayment plan.

Alternatives to Title Loans

Consider alternatives like personal loans, credit card advances, or borrowing from friends and family. These options might offer lower interest rates and more flexible repayment terms.

Benefits of Title Loans

Despite the risks, title loans in Mississippi offer benefits like quick access to cash and no credit check requirements. They can be a viable option in emergencies when other sources are unavailable.

Fast Access to Cash

One of the primary benefits of title loans is the speed at which you can obtain funds. In many cases, you can receive the money on the same day you apply.

No Credit Check

Since the loan is secured by your vehicle, most lenders do not require a credit check. This feature makes title loans accessible to those with poor or no credit history.

Repayment Terms and Options

Repayment terms for title loans in Mississippi vary. Understanding these terms is crucial to avoid losing your vehicle.

Typical Repayment Structure

Repayment periods can range from a few weeks to a month. Some lenders may offer longer terms, but this could result in higher interest costs.

Options in Case of Financial Difficulty

If you face difficulty repaying the loan, communicate with your lender immediately. Some lenders may offer refinancing or rollover options, albeit with additional fees and interest.

How Title Loans Affect Your Finances?

Title loans can have a significant impact on your financial health. The high-interest rates and risks associated with these loans can lead to long-term financial strain if not managed carefully.

Impact on Credit Score

While most title loan lenders don’t require a credit check, defaulting on the loan could still affect your credit score if the lender chooses to report it.

Long-Term Financial Implications

The high costs associated with title loans can create a cycle of debt, especially if you repeatedly roll over the loan. It’s crucial to consider the long-term implications on your financial stability.

Strategies for Responsible Borrowing

Responsible borrowing is key when dealing with title loans in Mississippi. It involves understanding your financial situation and the loan’s impact on it.

Assessing Your Financial Situation

Before taking a title loan, evaluate your financial health. Consider your income, expenses, and ability to repay the loan without jeopardizing your financial stability.

Planning for Repayment

Develop a realistic repayment plan. Consider your income sources and ensure you can meet the loan’s deadlines without causing financial distress.

Title Loan Lenders in Mississippi

Choosing the right lender is crucial. Mississippi has numerous title loan providers, each offering different terms and conditions.

What to Look for in a Lender

Look for licensed lenders with transparent terms and reasonable interest rates. Avoid lenders who practice predatory lending or have hidden fees.

Comparing Different Lenders

Research and compare different lenders. Consider factors like loan terms, interest rates, customer reviews, and additional fees.

Impact of Title Loans on Mississippi Residents

Title loans significantly impact Mississippi residents, especially those in financial distress. Understanding this impact helps in making informed decisions.

Economic Implications

For many Mississippians, title loans are a double-edged sword. They provide immediate financial relief but can lead to a cycle of debt due to high-interest rates.

Social Considerations

Title loans can exacerbate financial inequalities and affect vulnerable populations. Borrowers must be aware of these broader social implications.

Avoiding Predatory Lending Practices

Predatory lending is a serious concern in the title loan industry. Borrowers should be vigilant to avoid falling prey to such practices.

Recognizing Red Flags

Be wary of lenders offering loans without proper documentation, charging exorbitant fees, or not disclosing full terms.

Repayment Flexibility in Vehicle Title Loans

Understanding the flexibility in repayment terms for vehicle title loans is crucial for borrowers. Different lenders offer varying degrees of flexibility, which can significantly impact the borrower’s ability to repay the loan without undue stress.

Exploring Flexible Repayment Options

Some lenders may offer customizable repayment plans, allowing borrowers to align their loan payments with their financial situation. This flexibility can include varying the payment amounts or adjusting the payment schedule to match the borrower’s income cycle.

It’s vital for borrowers to inquire about these options before finalizing the loan to ensure they can meet their obligations without risking their vehicle.

Negotiating Terms with Lenders

Borrowers should not hesitate to negotiate the terms of their loan. Lenders might be open to modifying the terms, especially if it increases the likelihood of timely repayment.

Effective negotiation can lead to more manageable interest rates or a longer repayment period, which can be crucial for borrowers in preventing financial strain and avoiding the risk of vehicle repossession.

Vehicle Valuation in Title Loans

The value of the vehicle plays a pivotal role in title loans, as it directly influences the loan amount. Understanding how lenders determine this value can help borrowers gauge what to expect in terms of loan size and terms.

Methods of Vehicle Appraisal

Lenders typically use a combination of factors to appraise the value of a vehicle, including its make, model, year, mileage, condition, and market demand. They may use industry-standard guides like the Kelley Blue Book or NADA guides, or conduct an in-person inspection. Knowing how your vehicle is appraised can provide insight into the loan amount you might receive.

Maximizing Loan Amount Through Vehicle Care

Maintaining your vehicle in good condition can positively impact its appraisal value. Regular maintenance, addressing any mechanical issues, and keeping the vehicle clean can potentially lead to a higher valuation, thus increasing the potential loan amount. Borrowers should consider this factor when preparing to use their vehicle as collateral for a title loan.

Collateral Risks in Secured Loans

Using a vehicle as collateral in a secured loan like a title loan carries inherent risks. Understanding these risks is fundamental to making an informed decision about whether to proceed with such a loan.

Risk of Asset Loss

The most significant risk in a title loan is the potential loss of the vehicle. If the borrower is unable to repay the loan, the lender has the legal right to repossess and sell the vehicle to recover the loan amount. This can be particularly distressing if the vehicle is the borrower’s primary means of transportation.

Managing Collateral Risk

To manage this risk, borrowers should consider the loan amount carefully, ensuring it aligns with their ability to repay. Additionally, exploring insurance options that can cover the loan amount in case of unforeseen circumstances like accidents or theft could provide an extra layer of security.

Interest Rate Dynamics in Short-Term Lending

Interest rates are a critical component of any loan, and in the case of short-term lending like title loans, they can be particularly high. Understanding these rates and how they are calculated can help borrowers make cost-effective decisions.

Understanding APR and Interest Calculations

The Annual Percentage Rate (APR) is a key figure in any title loan agreement. This rate includes not only the interest but also any additional fees and charges. Borrowers should understand how the APR is calculated and what it means for their total repayment amount. Comparing APRs across different lenders can help in finding the most cost-effective option.

Strategies to Mitigate High-Interest Costs

To mitigate the impact of high-interest rates, borrowers should aim to repay the loan as quickly as possible. Shortening the loan term can significantly reduce the total amount of interest paid.

Additionally, borrowers should look out for any prepayment penalties and choose lenders that do not impose such fees, allowing them to pay off the loan early without extra costs.

Loan Renewal and Rollover Implications

Loan renewal and rollover are common practices in the title loan industry. While they offer temporary relief in repayment, they come with implications that borrowers should be aware of.

Understanding Rollover Terms

When a borrower is unable to repay the loan by the due date, some lenders offer the option to roll over the loan into a new agreement. This often involves paying additional fees and can lead to an increased interest rate, resulting in a higher overall repayment amount.

Risks of Continuous Rollovers

Continuous rollovers can trap borrowers in a cycle of debt, where they are perpetually paying fees and interest without reducing the principal loan amount. It’s essential for borrowers to consider the long-term financial impact of rollovers and avoid them if possible.

Seeking financial counseling or exploring alternative funding sources can be a more sustainable approach to managing financial challenges.

Can You Negotiate Terms with Vehicle Collateral Lenders?

Negotiating with lenders who offer loans against vehicle titles is an important consideration for potential borrowers. Understanding if and how you can negotiate can impact the terms of your loan significantly.

Exploring Negotiation Possibilities

It’s a common misconception that the terms of a loan secured by a vehicle are fixed and non-negotiable. In reality, many lenders are open to negotiation, especially if it increases the likelihood of loan repayment.

Borrowers should feel empowered to discuss terms such as interest rates, repayment schedules, and loan amounts. Effective communication can lead to more favorable terms, reducing the financial burden and risk of losing the vehicle.

Strategies for Successful Negotiation

To negotiate effectively, it’s crucial to be well-informed. Researching average interest rates and repayment terms can provide leverage. Additionally, presenting a solid repayment plan and demonstrating financial responsibility can make lenders more inclined to offer favorable terms.

Remember, negotiation is about finding a mutually beneficial agreement, so approach it with a cooperative mindset.

What Are the Risks of Defaulting on a Title-Based Loan?

Defaulting on a loan secured by a vehicle title carries significant risks. It’s important for borrowers to fully understand these risks before entering into a loan agreement.

Consequences of Loan Default

The most immediate risk of defaulting on a title-based loan is the loss of the vehicle. Lenders have the legal right to repossess the vehicle if the borrower fails to meet the repayment terms.

This can have a drastic impact, especially if the vehicle is essential for the borrower’s livelihood or daily activities. Additionally, defaulting can lead to additional fees and damage to the borrower’s credit score, if reported.

Long-Term Implications of Default

The long-term implications of defaulting on a title-based loan extend beyond the loss of a vehicle. It can result in a lasting negative impact on one’s credit history, making it more difficult to obtain loans in the future.

The financial strain of dealing with the aftermath of default, such as finding alternative transportation or dealing with debt collectors, can also have significant personal and economic consequences.

Is Refinancing an Option for Title Pledges?

Refinancing is an option often considered by borrowers of loans secured by vehicle titles. It can provide a way to manage high-interest rates or unmanageable repayment schedules.

Understanding Refinancing Terms

Refinancing involves taking out a new loan to pay off the existing one, potentially offering more favorable terms such as lower interest rates or extended repayment periods. It can be a viable strategy to avoid defaulting on a loan, especially if the borrower’s financial situation has changed since the original loan was taken out.

However, it’s important to be cautious, as refinancing can also lead to additional fees and, in some cases, higher overall costs.

Evaluating the Benefits and Risks

Before deciding to refinance, borrowers should carefully evaluate the benefits and risks. While refinancing can provide immediate relief, it can also extend the duration of debt and potentially lead to paying more in the long run.

It’s essential to compare different refinancing options and fully understand the new loan terms. Consulting with a financial advisor can also be beneficial in making an informed decision.

Are There Alternatives to Using Your Car as Loan Collateral?

Exploring alternatives to using a vehicle as collateral for a loan is an important consideration for those in need of quick funds but wary of the risks associated with title loans.

Other Loan Options

There are several alternatives to title loans that don’t involve risking a vehicle. Personal loans, payday loans, credit card cash advances, or borrowing from friends and family can be options, depending on the borrower’s credit score and financial situation.

Each of these alternatives has its own set of pros and cons, such as varying interest rates and repayment terms, that should be carefully considered.

Seeking Financial Advice

For those unsure about the best course of action, seeking advice from a financial advisor can be beneficial. They can provide guidance on the most suitable type of loan based on individual circumstances and help navigate the complexities of different financial products.

Additionally, non-profit organizations may offer free or low-cost counseling services, providing valuable insights into managing debt and financial planning.

Conclusion

In conclusion, title loans in Mississippi offer a quick and accessible financial solution, especially for those in urgent need of funds. However, the high interest rates and the risk of losing one’s vehicle make it imperative for borrowers to consider this option carefully. It’s crucial to understand the terms, abide by the state regulations, and have a solid repayment plan in place.

Responsible borrowing and awareness of one’s financial capabilities are key to ensuring that a title loan becomes a helpful resource rather than a financial burden. Ultimately, weighing the benefits against the risks and exploring other financial options can lead to more informed and safer financial decisions.

People Also Ask

What Are the Legal Limits on Interest Rates for Auto Title Loans in Mississippi?

In Mississippi, the legal limits on interest rates for auto title loans are strictly regulated. The state caps the interest rates to protect consumers from excessively high charges. Typically, these rates are governed by the Mississippi Title Pledge Act, which stipulates the maximum annual percentage rate (APR) that lenders can charge. It’s crucial for borrowers to understand these limits to avoid predatory lending practices. The exact rate can vary, so it’s recommended to consult the latest version of the Mississippi Title Pledge Act or a legal expert for the most current information.

Can I Extend or Roll Over My Car Collateral Loan in Mississippi?

Yes, in Mississippi, it is possible to extend or roll over a car collateral loan, but this comes with specific conditions and risks. The Mississippi Title Pledge Act allows for the renewal of a title loan, but each renewal can add additional fees and interest. This can quickly escalate the total amount owed, leading to a cycle of debt. It’s vital for borrowers to carefully consider the long-term financial implications of rolling over a title loan and to explore other alternatives if possible.

What Happens If I Default on a Title Loan in Mississippi?

Defaulting on a title loan in Mississippi can have serious consequences. If a borrower fails to repay the loan according to the terms agreed upon, the lender has the legal right to repossess the vehicle used as collateral. Following repossession, the lender may sell the vehicle to recover the outstanding loan amount. It’s important for borrowers to communicate with their lender if they anticipate difficulty in repayment, as some lenders may offer alternative repayment plans or extensions.

Are There Any Specific Documentation Requirements for Obtaining a Title Loan in Mississippi?

Yes, there are specific documentation requirements for obtaining a title loan in Mississippi. Typically, borrowers must provide a valid government-issued ID, proof of income, proof of residency, and most importantly, the original vehicle title showing clear ownership. Some lenders might also require additional documentation, such as vehicle insurance or references. Ensuring that all the required documents are in order can streamline the loan process.

How Quickly Can I Access Funds from a Title Loan in Mississippi?

The speed at which funds can be accessed from a title loan in Mississippi varies, but typically, borrowers can receive funds quite quickly, often on the same day of application. The fast processing time is one of the appealing features of title loans, making them a viable option for emergency financial needs. However, the exact timing can depend on the lender’s procedures and the completeness of the borrower’s documentation.

Muhammad Talha Naeem is a seasoned finance professional with a wealth of practical experience in various niches of the financial world. With a career spanning over a decade, Talha has consistently demonstrated his expertise in navigating the complexities of finance, making him a trusted and reliable figure in the industry.

Related posts:

Are Credit Card Skins Legal? All You Need To Know

Are Credit Card Skins Legal? All You Need To Know

My Chime Direct Deposit Is Late [All You Need To Know]

My Chime Direct Deposit Is Late [All You Need To Know]

Does Grubhub Accept Visa Debit Cards? Quick Answer

Does Grubhub Accept Visa Debit Cards? Quick Answer

Can I Rent A Car With A Chime Debit Card? [Learn The Facts]

Can I Rent A Car With A Chime Debit Card? [Learn The Facts]

How To Add Venmo Card To Apple Pay Without Card? 4 Steps

How To Add Venmo Card To Apple Pay Without Card? 4 Steps

Can I Become A Social Worker With A Business Degree? Answered

Can I Become A Social Worker With A Business Degree? Answered

Which Is A Characteristic Of A Business Opportunity? Answered

Which Is A Characteristic Of A Business Opportunity? Answered

What Bank Is PayPal On Plaid? A Complete Breakdown

What Bank Is PayPal On Plaid? A Complete Breakdown